The European real estate market is shifting its focus. After years of prioritizing returns, the market is now increasingly focused on the quality of the assets being financed. Against a backdrop of greater credit selectivity and less linear real estate cycles, the choice of the underlying asset class has become the true differentiating factor in real estate debt strategies.

Not all real estate segments, in fact, are capable of sustaining debt structures in a more complex and selective environment.

The new credit filter: structural demand and asset quality

According to analysis by JLL, capital is progressively concentrating on segments characterized by structural demand, high liquidity, and greater visibility of cash flows. This trend is also confirmed by the CBRE European Outlook report, which highlights how investors and lenders are favoring more defensive sectors, with lower exposure to macroeconomic volatility and a growing focus on asset quality and the stability of returns.

This translates into a paradigm shift: in this new equilibrium, the focus is no longer simply on financing a project, but on selecting asset classes capable of sustaining debt throughout the real estate cycle. This means financing the right asset classes.

The asset classes attracting credit today

It is in this context that the segments toward which capital is flowing clearly emerge. These are not necessarily those with the highest yields, but those that offer the best balance between risk and stability.

Residential—particularly high-end residential—student housing, alternative living, and selective hospitality share some key characteristics: solid demand, market depth, and greater predictability of cash flows.

These are the asset classes that today are not only able to attract investment but, above all, to support credit structures in an efficient and resilient manner.

Residential (especially luxury): global capital and resilient demand

Within the residential sector, the high-end segment stands out for its strength and ability to attract international capital.

According to Knight Frank’s Global Super-Prime Intelligence report for the fourth quarter of 2025, 555 transactions exceeding $10 million were recorded in major global markets, up 17% quarter-over-quarter, for a total value of $10.3 billion and an average transaction value reaching $18.6 million. For real estate debt, this translates into greater liquidity, greater protection, and greater predictability of cash flows.

Student housing and alternative living: unmet demand

Alongside traditional residential real estate, the importance of so-called “alternative living” is growing, with student housing as the most emblematic segment. According to JLL, in Italy the sector attracted approximately €500 million in investments in 2025, supported by extremely solid fundamentals: approximately 2 million students in the 2024/2025 academic year (+2.3% annually) and a 15% increase in international students, against an estimated supply of just 80,000 beds.

Even considering a significant development pipeline in the coming years, the gap between supply and demand will remain wide, continuing to support high occupancy levels.

According to CBRE, this segment ranks among those with the best growth prospects in the European landscape, alongside co-living and multifamily. For lenders, these are assets particularly suited to debt structures thanks to the visibility of revenues and the depth of demand.

Hospitality: Selective Recovery and Focus on Quality and the High-End Segment

Following the high volatility of the pandemic years, the hospitality sector has returned to investors’ radar, but with a very different approach compared to the past. Capital is now concentrated on high-end assets located in prime destinations, with a strong ability to attract international demand and sustain high pricing levels.

According to JLL, the luxury and upper-upscale segment is the one showing the best performance in terms of ADR (Average Daily Rate), thanks to its ability to capture demand that is more resilient and less sensitive to economic cycles.

In this context, hospitality becomes an opportunity for real estate debt only if carefully selected, prioritizing assets with solid fundamentals and distinctive positioning. In practice, hospitality is no longer a cyclical bet, but a targeted investment in assets with pricing power and strong international demand.

The common thread: predictable cash flows and downside protection

When looking at these asset classes as a whole, a common element emerges: they are not necessarily those with the highest returns, but those with the best balance between risk and stability.

Luxury residential, student housing, alternative living, and selective hospitality thus share certain common characteristics, including structural demand, high occupancy or liquidity, and greater protection during periods of stress. And this is precisely what lenders are seeking today.

The Yeldo Strategy: Focus on Living and Underlying Quality

Yeldo’s strategy consistently reflects this market evolution. In 2025, the platform reached approximately €1.8 billion in total transaction volume and around 70 deals, consolidating its position in the European real estate market.

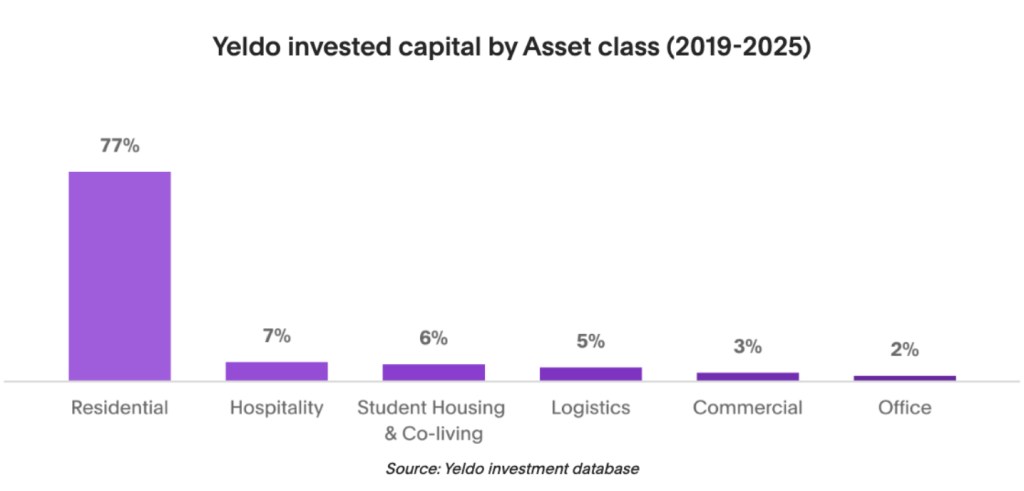

From an allocation perspective, the portfolio showed a clear concentration on the most resilient asset classes, with 77% invested in residential—of which approximately 61% is in the high-end segment—and growing exposure to student housing, co-living, and selective hospitality.

Specifically, the invested capital is distributed as follows: 77% in residential, 7% in hospitality, 6% in student housing and co-living, 5% in logistics, 3% in retail, and 2% in office.

Residential assets therefore form the core of Yeldo’s track record, with a strong focus on high-end projects, which have historically proven to be among the most resilient across various market cycles. But that’s not all: as explained above, capital has also been selectively invested in adjacent asset classes such as hospitality and student housing/co-living, as well as logistics and retail. More than mere diversification, this has been a strategic reallocation toward assets characterized by structural demand and greater stability of cash flows.

In terms of geographic distribution, activity has been concentrated primarily in Italy, a market that accounts for 58% of capital invested between 2019 and 2025. The remainder of the portfolio is distributed across other European markets, including Switzerland (17%)—which saw capital employed grow by approximately 30% in 2025 compared to the previous year—Spain (8%), Monaco (7%) and Portugal (6%), as well as smaller exposures in Liechtenstein (1%) and Luxembourg (1%).

Where Real Estate Debt Will Play Out in the Coming Years

The European real estate debt market is not slowing down: it is becoming more sophisticated.

Today, the real difference is no longer determined solely by the financial structure, but by the quality of the property underpinning it.

In this new landscape, the asset classes that truly perform are those capable of combining real demand, resilience, and cash flow visibility. And it is precisely on these fundamentals that real estate debt performance will be built in the coming years.